What Is Financial Macroeconomics? When the Economy Meets the Markets

· 23 min read

On the first Friday of every month, at 8:30 in the morning, Washington time, the U.S. Labor Department releases a single number: the jobs created over the month just ended. In the milliseconds that follow, sums measured in hundreds of billions change hands. Index futures plunge or soar, the yield on government bonds shifts by several hundredths of a point, the dollar strengthens or gives ground against the euro and the yen. And yet nothing has moved in the tangible world since the night before: the same factories are running, the wages already paid are no more paid than they were, the goods on the shelves carry the same price tags. What has just happened is of another nature entirely. A piece of information about the economy has entered the system, and the price of almost everything that trades has instantly readjusted to take it into account.

It is in that gap of a few seconds, between a data point and its shock wave, that the subject of this journey resides. Financial macroeconomics is the study of that crossing: the way the state of an economy — and still more the trajectory people ascribe to it — translates into asset prices; and, reciprocally, the way those prices end up bearing down on the very economy that gave rise to them. The title of this article captures its spirit. There is, on one side, the economy, slow and tangible; on the other, the markets, fast and abstract; and between the two, a permanent meeting point that the whole challenge is to learn to read.

The economy on one side, the markets on the other

We speak of the economy and the markets as though they were one and the same thing, and the confusion is so widespread that it deserves to be cleared up from the outset. The real economy is the realm of production and use: firms make goods and provide services, employees earn an income they spend or set aside, a state levies taxes and redistributes. It unfolds over the long horizon of quarters and years, because one does not open a factory or train a workforce in an afternoon. We measure it through aggregate quantities — total output, the general level of prices, the share of working-age people without a job — that sum up, in a handful of figures, the activity of millions of agents.

Financial markets are of an altogether different fabric. What is traded there is not present goods but claims on the future. To buy a share is to acquire a fraction of the profits a firm will generate over the decades to come; to hold a bond is to be promised a stream of future payments; to take a position on a currency is to wager on the relative value of two economies at a given horizon. Because the object of exchange is the future, and because the future reshapes itself with every new piece of information, the price of these claims is revised continuously, by the second. Where the economy walks, the markets run.

From this difference in nature follows a difference in function that must be grasped clearly, for it governs everything else. A market price is not a passive thermometer; it is a mechanism for aggregating information. When a buyer and a seller agree on a price, they condense into that single figure everything they believe they know, hope for, or fear about the asset's future. The resulting price synthesizes thousands of scattered judgments into one observable quantity. This is what makes markets such a singular object for the macroeconomist: they offer him, in real time and in numbers, the collective opinion about tomorrow's economy — an opinion that is fallible, sometimes herd-like, but always instructive.

A discipline of junction

Macroeconomics, taken on its own, studies the economy at the scale of the whole: what determines the wealth a country produces, why prices rise faster or slower, what makes unemployment swell or recede, how money circulates and at what price one borrows. It reasons in terms of masses — household consumption, business investment, government spending, trade with the rest of the world — and in terms of the institutions that orchestrate them, foremost among them the central bank. It is the science of the forest rather than the tree: it has no interest in knowing why a particular household bought a particular car, keeping only the overall movement of spending.

This science has existed for close to a century, but the idea of wiring it directly to asset prices is more recent, and less obvious, than it might seem. For a long time, economic thought held money and finance to be a veil draped over the real economy: a convenient mechanism, neutral in the long run, that did not alter the substance of things. It took the upheavals of the twentieth century to undo this separation:

- Keynes, in the 1930s, placed the expectations and psychology of investors — his famous "animal spirits" — at the heart of what determines investment, and therefore activity.

- The monetarists, Milton Friedman foremost among them, reminded everyone that excessive money creation always ends up being paid for in inflation.

- The rational expectations revolution, in the 1970s, showed that one could not reason about an economy without assuming that its agents anticipate the policy about to be enacted and adjust to it in advance.

- The efficient market hypothesis, at the same moment, asserted that prices already incorporate all available information.

From the meeting of these currents was born the contemporary way of linking macro to markets: central banks that steer the economy by targeting a level of inflation, and markets that spend their time anticipating those central banks' reactions. Financial macroeconomics is the heir to that history.

Delimiting its scope amounts to drawing two boundaries. On one side, it differs from pure macroeconomics, which can content itself with explaining growth or inflation without ever asking what the markets will make of them; financial macroeconomics, by contrast, never loses sight of that question. On the other side, it parts ways with corporate financial analysis, which dissects a balance sheet or values one particular company: its object is not this or that security, but the common backdrop — rates, inflation, the cycle, liquidity — against which all securities are valued at once. Between the macro that ignores markets and the finance that ignores macro, it occupies the hyphen; and that hyphen, as we shall see, is travelled in both directions.

Why an inflation number is worth billions

How can a mere statistic move billions in a few seconds? To understand it, we first need to know how the price of a financial asset — a share, a bond — is set. The idea fits in one sentence: the price of an asset is the sum of the income one hopes to draw from it later, brought back to what it is worth today.

Two elements are enough for this calculation:

- The expected future income: what one hopes to collect in the years to come — a company's profits, a bond's interest, a building's rents.

- The discount rate: the "conversion rate" that turns those future sums into present value.

Why must we convert, instead of taking the future sums as they are? Because a euro received later is worth less than a euro received right now. And this for three concrete reasons:

- Investing it. The euro you already have in hand can be invested today and made to grow; the one you will only receive in ten years deprives you, in the meantime, of all that interest. Waiting has a cost.

- Inflation. Over time, prices rise. €100 will buy fewer things in ten years than today: the same sum, received later, has weaker purchasing power.

- Uncertainty. A distant promise may not be kept — the company goes bankrupt, the borrower fails to repay. The money you already hold, by contrast, is certain.

The more distant the maturity, the more these three forces operate, and the more the promise loses of its present value. To convert is precisely to account for this.

The simplest way is to picture a fraction: the future income on top, the discount rate on the bottom.

- Anything that raises the top (better expected profits) raises the price.

- Anything that raises the bottom (higher rates) lowers the price.

Those are the two levers. And the economy acts on both.

The top of the fraction — income — depends on the health of the economy. When activity is strong, firms sell more, profits climb, defaults grow rare; a recession produces the opposite. A good growth figure, then, is the top of the fraction appreciating.

The bottom of the fraction — the rate — depends above all on interest rates and inflation. And interest rates are largely steered by the central bank. When it raises them to cool inflation, the bottom of the fraction swells, and asset prices fall mechanically.

A worked example makes all this concrete. Someone promises you €100 in one year. How much would you agree to pay today for that promise?

Surely not €100. Because €100 you already have in hand, you can invest: at a risk-free rate of 4%, it becomes €104 in a year. Handing over €100 today only to get back €100 in a year would therefore be a bad deal. The fair price is the sum that, invested at that rate, gives back exactly €100 after one year.

- At 4%, that sum is about €96: invested at 4%, €96 becomes €100 in a year. The promise is therefore worth ~€96, not €100.

- At 8%, you need only €93 to arrive at the same €100. The same promise is suddenly worth no more than ~€93.

We have changed nothing about what will be received — still €100 — : only the rate has moved, and the present value has fallen. Over one year, the gap looks tiny, barely €3. But it swells fast over time, because the rate applies every year, compounding on itself. The same promise of €100 in thirty years is worth about €31 at 4%… but barely €10 at 8%: moving from one rate to the other divides its present value by three. This is why a seemingly minuscule rate increase can wipe out billions on the assets whose income lies furthest off.

One last point about that rate: it does not boil down to the risk-free yield. No one takes on risk for free. To accept an uncertain future, investors demand a return higher than that of a safe investment — this supplement is called the risk premium, and it adds to the rate, hence to the bottom of the fraction. The more threatening the future appears, the higher the premium: during a recession or a crisis, it climbs, weighs down the bottom of the fraction, and therefore pushes prices lower. An economic blow thus strikes risky assets twice: it reduces expected income (the top falls) and it raises the price of risk (the bottom rises). Two blows, in the same direction: downward.

Key takeaway — An asset's price ≈ expected future income, on top of a fraction, divided by the discount rate, on the bottom. The economy acts on both at once: nearly every asset price is, without saying so, a double bet — on growth and on rates.

This is what makes the subject subtle: a single piece of news can improve expected profits (the top rises) while also pushing rates up (the bottom rises too). The two effects work against each other, and the final result on the price is anything but obvious. That is why this mechanism so often disconcerts beginners — and why it is so fruitful once understood.

Not all assets react with the same force. It all depends on the timing at which one collects one's income: the more distant it is, the more its present value is jolted by the slightest move in rates — exactly as in the €100 example, where one point of rate weighed far more heavily over thirty years than over one. Financiers have a word for this sensitivity: duration. Think of it as an asset's "exposure to the wind" of interest rates: the further off its income, the greater the exposure.

It can even be approximated by a number. Expressed in years, duration roughly gives the percentage of value a security loses when rates rise by one point. Before illustrating this, a word on two terms that will be useful. A bond is a loan: by buying it, you lend your money to a state or a company, which undertakes to pay you interest for a set period, then to repay the sum lent at maturity — in 2 years, 10 years, 30 years… It is therefore an asset whose payment schedule is known in advance, which makes it the ideal example for talking about duration.

- A 2-year bond has a duration close to 2: a one-point rise in rates costs it only about 2% of its value.

- A 30-year bond has a far higher duration — on the order of 20 if it pays large interest along the way, and up to 30 if it pays nothing before maturity: the same one-point rise then costs it 20% to 30%, ten times more, or even more.

The gap between these last two figures is no detail: duration is not quite the same as maturity. For equal maturity, the earlier a bond pays out, the shorter its duration — because it is the moment the money comes back, not the repayment date alone, that counts.

The same intuition extends to equities, but only qualitatively. To hold a share is to own a small part of a company, and therefore a claim on its future profits; the dividend is the fraction of those profits it pays out to its shareholders each year — the income a share generates as long as one holds it. A growth stock, which reinvests everything today and promises its big profits for a distant future, reacts far more strongly to a rate increase than a mature company already paying steady dividends. One caveat, however: on a share, the income is neither fixed nor dated in advance, so one cannot assign it a duration figure as clean as on a bond. Here, "high duration" simply means "very sensitive to rates, because the bulk is expected later" — an apt image, not an exact measure.

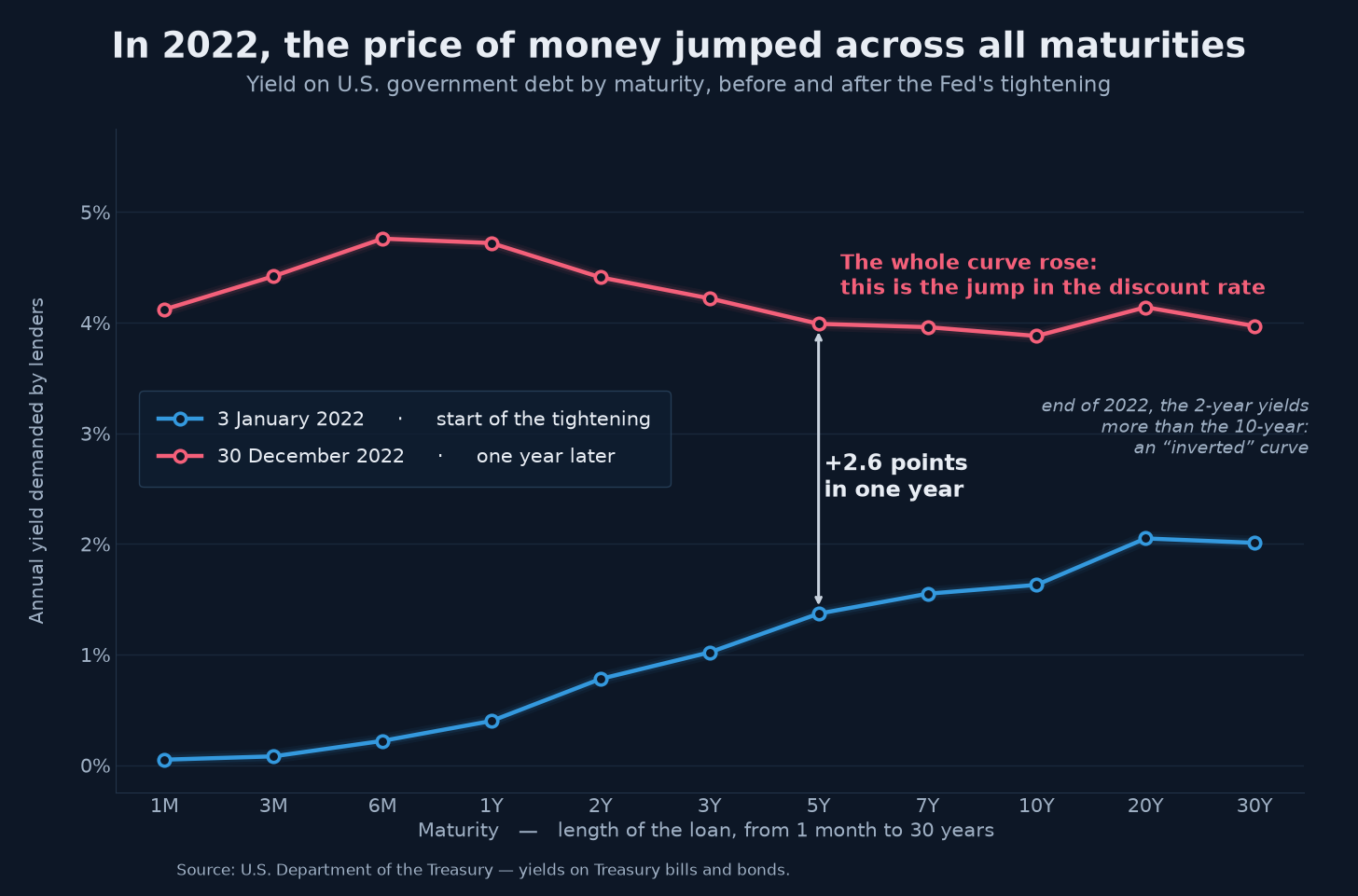

The year 2022 gave a brutal demonstration of this. To break an inflation that had returned to a peak unseen in forty years, the U.S. central bank raised its policy rate from near 0% to more than 5% in a few months — the fastest tightening since the early 1980s. The assets most sensitive to duration — tech stocks with distant profits, long bonds, speculative assets with no income — were the hardest hit. Not because the real economy had collapsed, but because the rate that discounts their future had changed completely: the top of the fraction still held; it was the bottom that swept everything away.

To take in this shock at a single glance, one uses the yield curve. The principle is simple: for each loan maturity — one month, two years, ten years, thirty years — one notes the rate the market demands today to lend to the state over that horizon, then connects the dots. The result is a curve that sums up, in one line, the price of money at every maturity. Comparing it between the start and the end of 2022 shows the scale of the shock in a single image.

Each curve connects the rate demanded to lend to the U.S. government according to the length of the loan, from one month to thirty years. Over one year, the entire line rose by several points: it is this jump in the discount rate — the "bottom of the fraction" — and not a drop in profits, that struck the assets with the most distant income. One detail is worth the eye: normally, lending for longer pays more, and the curve rises from left to right; but at the end of 2022, the 2-year rate exceeded the 10-year rate — the curve had "inverted." This rare situation, in which a short loan pays more than a long one, is usually taken as a signal of a coming recession.

The market prices the gap, not the level

Once we accept that prices discount the future, a consequence follows that disconcerts almost everyone starting out, and that can never be repeated often enough. Markets do not react to the level of a number, but to its gap relative to what was expected. A company can report a spectacular jump in profits and watch its share price plunge in the aftermath, simply because the market had hoped for even better and had, for weeks, been buying the stock in that expectation. The good news was already in the price; only the disappointment was not. What trades, at the moment of the release, is not the news itself but the distance between the news and its anticipation.

Professionals have a name for that anticipation: the consensus, the average of the forecasts the market has formed ahead of the release and around which it has positioned itself. If the data comes in line with the consensus, prices barely move, because the bulk had already been discounted; if it beats or disappoints, they readjust all the more sharply as the surprise is large. This is the idea behind the old trading-floor adage: buy the rumor, sell the news — by the time the awaited event materializes, those who had anticipated it have already taken their profits. It is not a law, more a conditional tendency: the effect only plays out when the market had positioned itself strongly in the direction of the rumor, and it regularly reverses when the news surprises beyond what was already in the prices. The deeper lesson, though, always holds: what everyone already knows can no longer be earned. A widely announced recession is, for a good part, built into prices well before it shows up in the statistics, and it is the news that deviates from the accepted scenario, not the news that confirms it, that makes market history.

We should, in fact, be precise about what the market anticipates exactly, for it is not a point but an entire trajectory. At any moment, prices incorporate an expected path: not today's policy rate, but the sequence of rates the central bank is supposed to set in the months and years ahead, as one can read it in the futures contracts — those instruments where numerical bets on tomorrow's rates are traded today. A statement, a press release, an inflation figure move the markets only insofar as they alter that anticipated path. And because that path depends on the central bank's future decisions, which it makes based on the economy while watching the markets to gauge the effect of its own policy, a hall of mirrors sets in where each tries to get ahead of the other: the central bank watches markets that are only trying to second-guess it. The end of 2023 gave a clear illustration of this. Before the institution had cut a single rate, the markets, betting on imminent easing, drove yields down and stocks up with such force that financing conditions loosened of their own accord, at the risk of reviving the very inflation the tightening was meant to extinguish. The anticipation of policy was already producing the effects of policy.

The mirror acts on what it reflects

One might be tempted to stop there and treat the markets as the reflection — faithful or distorted — of an economy that would run its course independently of them. That would be to miss half the picture. Asset prices do not merely record the economy; they act on it in return, and it is this loop that makes financial macroeconomics something other than mere barometer-reading. This feedback travels through three main channels:

- Wealth. When the stock market and real estate rise durably, the households that hold them feel richer and loosen their purse strings; when those markets fall, they close their wallets.

- Credit. As soon as rates and the premiums lenders demand rise, borrowing costs more, investment projects are postponed, home purchases abandoned, and activity slows without any public decision having been taken to that end.

- The exchange rate. A currency that appreciates weighs on exporters and imports disinflation, while a currency that weakens does the opposite.

Together, these forces — the level of equities, the cost and availability of credit, the exchange rate, but also long-term rates and strains on funding — form what is called financial conditions, and we now have indices that try to sum them up in a single figure, so much do they govern the momentum of the real economy.

This feedback has an implication that beginners rarely suspect: a central bank does not steer the economy directly, but through the markets. Strictly speaking, it sets only a very short-term rate; everything else — the ten-year yield that serves as a benchmark for mortgages, the terms on which firms fund themselves, the level of stock markets — is determined by the markets, according to what they anticipate of future policy. This reality is sometimes captured in a formula: it is not the central bank that sets your mortgage rate, it is the bond market. The tightening of 2022 and 2023 only produced its effects by passing through this relay; and when, at the end of 2023, the markets loosened financing conditions faster than the institution wished, it found itself thwarted by the very mirror in which it sought to act.

What macro makes possible, and what it forbids us to hope for

An honest presentation of the discipline must state its limits right away, lest it promise what it cannot deliver. Understanding how the economy moves the markets confers no power of short-term prediction, and the opposite is in fact true: the better known and accepted a macroeconomic relationship is, the less it lends itself to being exploited, since the markets have already built it into their prices. Financial macroeconomics lights up the set; it does not whisper the line.

Recent years have driven this home with a salutary cruelty, by belying several regularities thought to be set in stone:

- The inversion of the yield curve — when borrowing short-term costs more than long-term — has for decades been taken as the most reliable harbinger of recession; it inverted durably from 2022 onward, and the recession that so many commentators announced did not arrive on the usual schedule.

- The alliance between stocks and bonds, on which the classic balanced portfolio rests, is supposed to cushion shocks: when one falls, the other usually rises and offsets it. In 2022, both fell in concert, because it was inflation and the rate rise striking them simultaneously, and the portfolio reputed to be prudent had one of its worst years in a century.

These rebuttals are not accidents to forget: they teach that macroeconomic regularities are historical tendencies, sensitive to the regime, and not mechanical laws.

There is a deeper reason for this, peculiar to markets and foreign to the natural sciences. A planet does not change its trajectory because astronomers have predicted it; a market, by contrast, changes its behavior the moment a regularity is spotted and exploited by enough participants. Collective belief in a scenario moves prices and, in doing so, undoes the scenario or hastens another. This reflexivity — the fact that expectations act on the reality they anticipate — forbids treating a macroeconomic forecast as one would a weather forecast. It explains at the same time why so many forecasts, even rigorous ones, turn out wrong, and why trying to move in and out of markets according to one's views — the temptation of market timing — impoverishes portfolios more surely than it enriches them.

What use is it, then? A great deal, provided one expects of macro what it can give. It does not serve to guess the next move, but to know what world one is investing in: a regime of high or low inflation, of rising or falling rates, of expansion or contraction, calls neither for the same assets nor for the same risks. It teaches one to recognize, in a piece of news, what was already expected and what genuinely surprises. Above all, it helps one not give in to panic or euphoria at the worst moment, which, over the span of a saver's life, is worth many a forecast. The right posture is not to bet on a single scenario, but to build a portfolio that withstands several; and it often happens that the wisest response to a macroeconomic forecast, however convincing, is to change nothing at all.

The map of the journey

It remains to place this article within the voyage it opens. Everything just sketched in broad strokes will be taken up, broken down, and illustrated across the modules, in a progression that goes from the most elementary to the most complete:

- The building blocks: growth and the wealth we measure through gross domestic product, money and the way it is created, inflation and the expectations that feed it, and finally the interest rate, that price of money which links all the others.

- The dynamics: the economic cycle and its breathing, the labor market whose tensions govern wages, the indicators investors scrutinize, and the central banks whose every word must be decoded.

- Macro wired to the markets: government debt and its weight on rates, the international dimension and the circulation of global liquidity, financial crises and the credit mechanics that engender them, and finally the way the great economic regimes govern the allocation of a portfolio.

- Practice, lastly, with an analyst's dashboard and a few tools to automate the monitoring.

So that none of this stays abstract, a single episode will serve as a thread from end to end: the sequence running from the shock of the pandemic, in 2020, to the soft landing of 2024–2025. In it we will find, condensed into five years, nearly all the phenomena the discipline studies: the collapse and then the rebound of activity, the return of an inflation thought to have vanished, the most brutal monetary tightening in a generation, the disinflation that followed, and markets that got it wrong as much as they saw it right. Each concept will be anchored, in its turn, in a precise episode of this story; and we have already glimpsed why this period makes such a precious case study: because it has, better than any theoretical lesson, proven our certainties wrong.

The essential thing, for now, fits in one sentence worth carrying along: an asset price is an opinion about the future of the economy, revised endlessly as that future comes into focus, and capable in return of altering the present. Everything else — growth, money, inflation, rates, central banks — is just a way of informing that opinion. The next chapter starts from there to answer the question that naturally arises: if markets already discount the economy, why does an investor need to understand it at all? The answer, as we shall see, is anything but obvious.