Why an Investor Needs to Understand the Economy: The Starting Intuition

· 21 min read

In January 2010, two savers invest the same sum and promise themselves not to reopen the account for fifteen years. The first spends the decade bent over the economy: he reads every jobs report, pores over central-bank statements, shifts his money according to his convictions — trimming as the storms he believes he sees approach, buying back when the horizon looks clear to him. The second does none of this: he buys a fund that tracks the entire world market, stops opening his statements, and devotes his energy to something else. Fifteen years pass. In the overwhelming majority of cases, it is the second who ends up with the larger capital. The first, by dint of having been right too early or too late, of having sold the day before the best sessions and bought back just before the worst, has paid dearly for his activity.

There is something cruel about the scene, for it seems to hand down a verdict without appeal: not only would understanding the economy have served no purpose, but using it to act would have done harm. And behind that verdict stands a respectable theory — the one the first article of this journey laid out. Markets already incorporate everything we know; they react not to the level of a number but to its gap with what was expected; and they change their behavior the moment a regularity is spotted and exploited by enough participants. If everything one can learn about the economy is already in the prices, why learn it? That is, word for word, the question on which the previous chapter ended.

This article's answer fits in a single sentence, and it overturns the intuition we spontaneously form: yes, the investor needs to understand the economy — but not for the reason the beginner believes. Not to guess the next number, not to beat the market at its own game, a contest largely lost in advance. For something quieter, sturdier and, in the end, far more useful: to know which world he is investing in, to see the real risks he carries, and to keep a cool head when everyone else loses theirs. This is the starting intuition of the whole voyage — the one that justifies the chapters to come by showing that their usefulness is nothing like what one imagines.

Being right is not enough to make money

We must begin by taking the objection seriously, for it is correct — at a certain level. The mechanism set out in the first article leaves little room for doubt: a price is an opinion about the future, revised continuously; it moves on the gap between the news and its anticipation, not on the news itself; and any well-known relationship is already discounted. The consequence, for anyone who dreams of winning by forecasting, is unpleasant: he is playing a step behind. To prevail, he would need not to be right, but to be more right than the consensus — that is, better than the whole body of participants combined, many of whom do this for a living and are better equipped than he is.

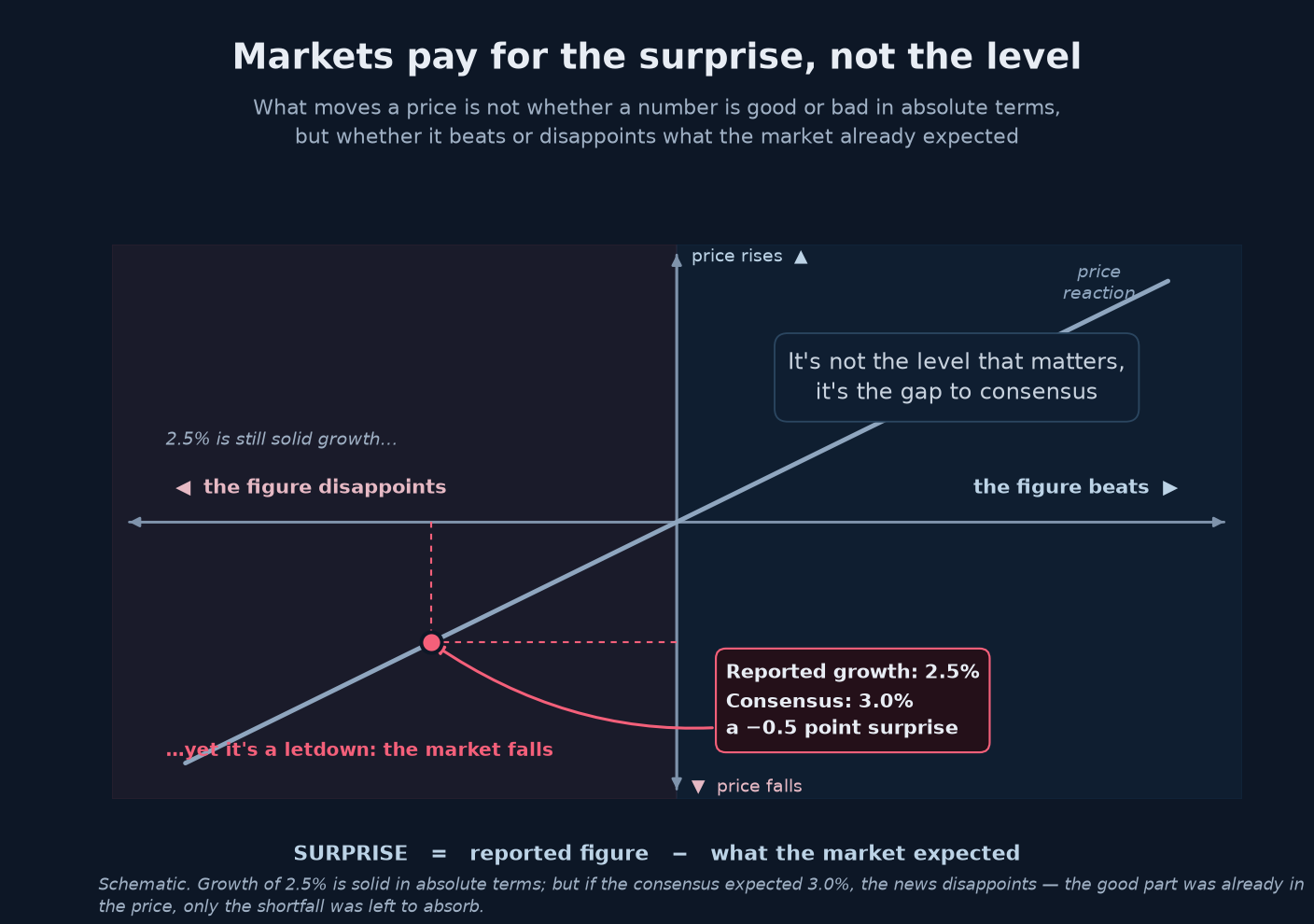

An example makes it tangible. Suppose you have done your homework and are convinced that U.S. growth will be strong this quarter. You are right: the figure comes out well above the previous one. And yet, at the instant of release, the market falls. Why? Because the consensus hoped for better still, and for weeks buyers had positioned themselves on that hope. Picture a consensus at 3.0% and growth that finally prints 2.5%: a solid number in absolute terms — an economy growing at two and a half percent is doing well — but a disappointment relative to what was already in the prices. You were right about the economy and wrong about the trade: the good news was already paid for; only the disappointment was not. Being right about the economy and making money in the market are two distinct things, and the first never guarantees the second.

The market does not reward the level of a number, but its gap to the consensus. Growth of 2.5% reported when 3.0% was expected is good news in absolute terms — and yet a disappointment: the hoped-for rise was already in the price, only the negative surprise was left to absorb.

This is no anecdote; it is a massive regularity. Decades of data say the same: over long horizons, a large majority of professional managers — paid precisely for this — do worse than a simple index that merely holds everything and forecasts nothing. And studies of how ordinary investors behave add a second finding: those who move in and out according to their macroeconomic convictions, who try to time the market, almost always lower their returns. Hence the adage all this eventually crystallized into: time in the market beats timing the market.

There is even a paradox here that theory knows well: as soon as a piece of public information is genuinely useful and everyone can seize on it, it is instantly built into prices and ceases to be useful. The macroeconomic knowledge shared by all neutralizes itself as a source of easy gains: precious for understanding, sterile for speculation. So let us grant the objection without flinching: macroeconomics is not a crystal ball, and whoever sells it as one is mistaken or is deceiving you.

But to conclude from this that it is useless would be a far deeper error, for it confuses two things that have almost nothing to do with each other: predicting the market and understanding the world in which one invests. The whole rest of this article works to separate them — and to show that the second remains indispensable even when the first is out of reach.

Climate, not weather

No meteorologist will tell you with certainty whether it will rain three weeks from now: the atmosphere is chaotic, and beyond a few days a forecast is barely better than chance. Yet no one concludes that knowing the climate is useless. One does not grow the same crops, build the same houses, or pack the same suitcase in the tropics and in the tundra. Tomorrow's weather is unpredictable in detail; the climate is decisive in the aggregate.

Markets follow the same score. The move of the day — the equivalent of weather — is dominated by surprise and noise, and remains largely unpredictable: that is all the previous section just established. But the climate is another matter. There exist, in macroeconomics, durable configurations of growth and inflation that settle in for quarters or years, that evolve slowly, and that determine which assets prosper and which suffer. These are the regimes, and it is they, not the next number, that the investor truly has an interest in learning to read.

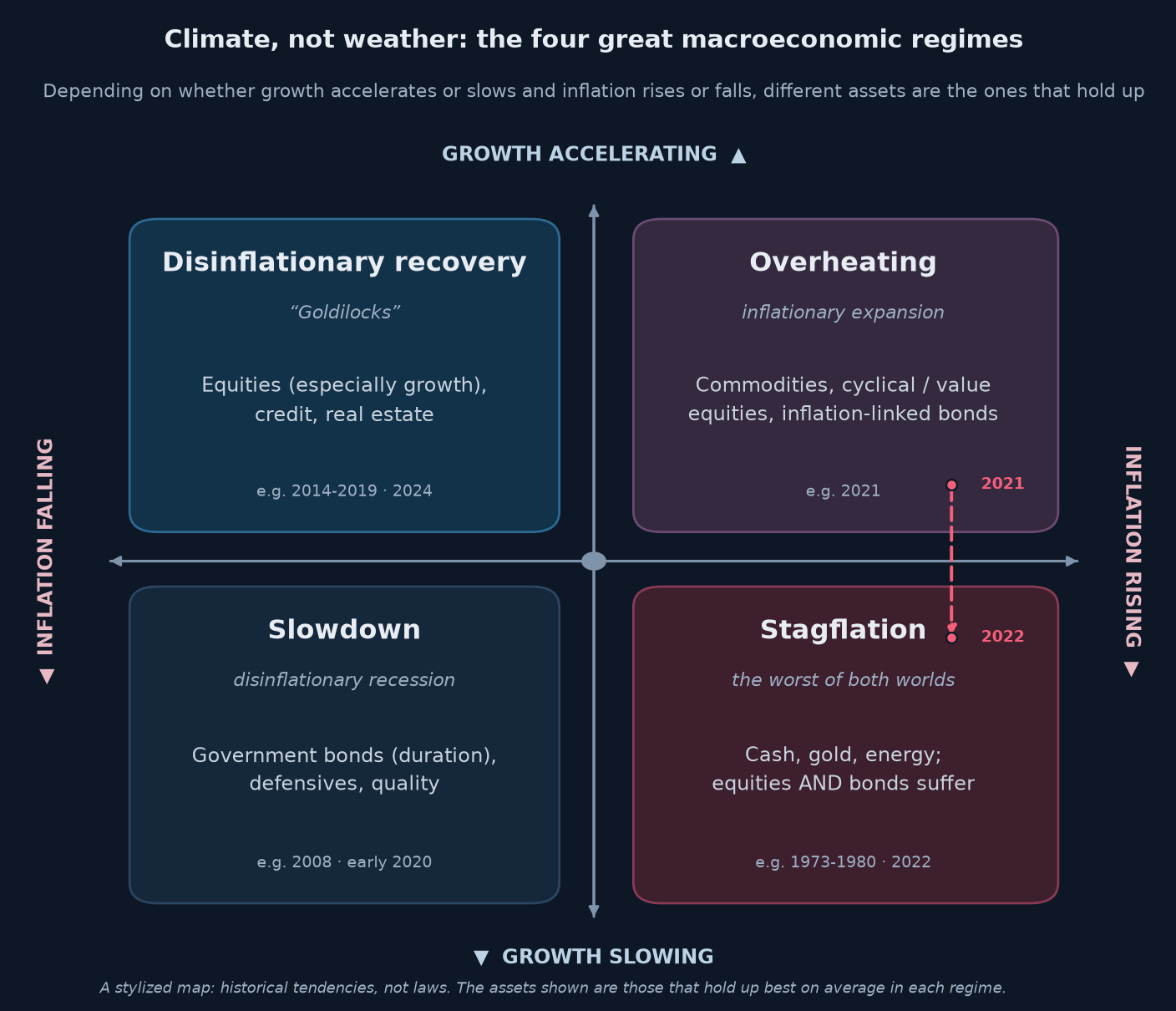

They are often boiled down to four great cases, according to whether growth is accelerating or slowing and inflation is rising or falling.

Each box answers to a growth-inflation pairing. In the "Goldilocks" recovery, the economy accelerates without prices running away: equities — above all those whose profits lie far off — and credit prosper. In overheating, growth and inflation climb together: commodities, cyclical equities and inflation-linked bonds come out ahead. In a disinflationary slowdown, everything subsides: government bonds, whose value rises as rates fall, and defensive stocks offer the best shelter. There remains the worst of worlds, stagflation — stalled growth, stubborn inflation — where equities and bonds suffer in concert, and only cash, gold and energy hold up. The map is deliberately simplified: these are historical tendencies, not laws, and the borders are blurred. The arrow recalls a recent shift: from the overheating of 2021, the economy slid in 2022 toward stagflation, growth rolling over while inflation stayed high.

The essential point is this: a regime is not forecast day by day, it is recognized, and it persists. There is no need to guess Friday's session to know which regime of growth, inflation and rates one is living in. And that single piece of knowledge — knowledge of climate, not of weather — changes everything about the positioning that fits, far more than any conjecture about the month's figure. The beginner believes that understanding the economy serves to anticipate the next data point; he would do better to see in it the means of answering a far more useful question: which climate am I investing in, and is it turning?

The contrast between two recent regimes makes the stakes concrete. Through the 2010s, inflation was absent and rates were pinned near zero: it was the golden age of growth stocks, whose distant profits a near-zero discount rate flattered, of long bonds, and of the 60/40 portfolio that married them. From 2022, the regime flipped: inflation back, rates surging — and the very assets the old climate had rewarded became the most exposed. Nothing in the day-to-day was predictable; but the change of climate, once recognized, said more about how to be positioned than a thousand forecasts of the next number ever could.

Honesty requires an immediate qualification. Regimes do not announce themselves: they are often named only after the fact, their boundaries are uncertain, and a regime can remain for a time poorly appraised by markets precisely because it changes slowly. But that is exactly where understanding the economy has the most to offer — on the slow variable that the fast machine of prices is sometimes late to absorb. Let us keep for now that recognizing one's climate is not predicting the weather, and that it is already an altogether different business.

Every portfolio is a macro bet that doesn't know it

The first article closed on a phrase that must now be unfolded: nearly every asset price is, without saying so, a double bet — on growth and on rates. Let us draw the conclusion that imposes itself. Every portfolio, however it was assembled, is a bundle of implicit macroeconomic bets. The saver who declares "I take no interest in the economy" has not freed himself from macro: he has merely stopped looking at the bets he holds. He is not without bets — he is blind to his own.

The danger has a name: hidden concentration. A portfolio can look diversified — many lines, many names — while all its lines depend, at bottom, on the same macroeconomic variable. True diversification does not consist in holding many things; it consists in holding things that do not all sink together when a single variable starts to move. And one cannot tell the first from the second without understanding the economy that links them.

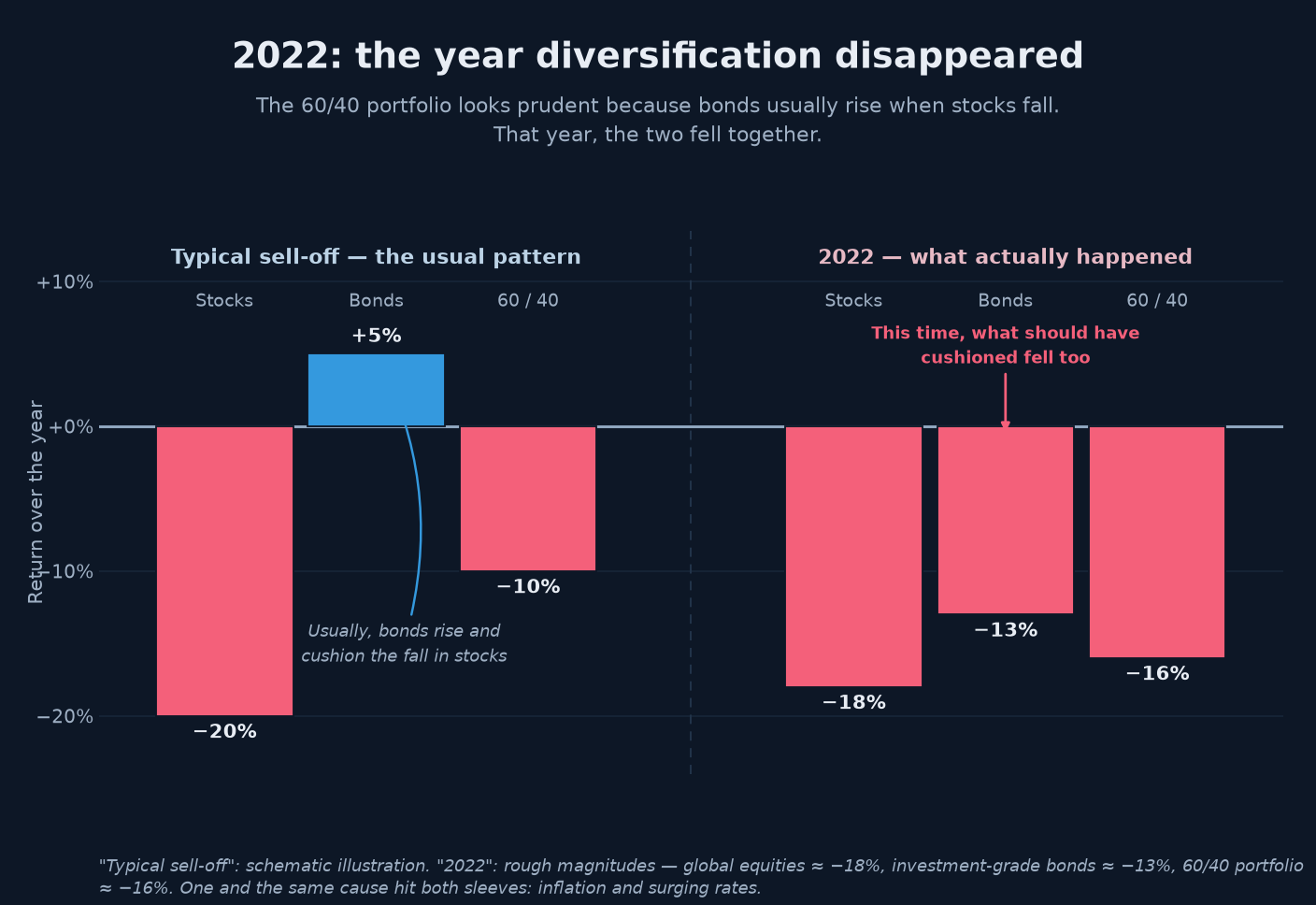

The year 2022 gave the brutal demonstration. The balanced portfolio par excellence, the famous 60/40 — sixty percent equities, forty percent bonds — passes for prudent because, ordinarily, when stocks fall bonds rise and cushion the blow. That year, both fell in concert: equities by nearly 18%, high-quality bonds by around 13%, one of the worst years in a century for that allegedly sensible allocation. Why? Because what struck them was one and the same cause: inflation and the surge in rates. The two pockets thought to be "different" were at bottom the same duration bet, the same wager on rates that would stay low. The diversification was an illusion — one that only a macroeconomic reading could pierce, not by forecasting the rate hike, but by seeing that the two compartments shared a single hidden risk.

Diversification by the sheer number of lines is an illusion once all the lines depend on a single variable: in 2022, stocks and bonds fell in concert, struck by inflation and the surge in rates — a single duration bet that didn't know itself.

Key takeaway — Whoever ignores the economy does not hold a portfolio free of macro bets: he holds one whose bets he cannot see. And one cannot manage a risk one cannot see. Understanding the economy is, first of all, the only way to know what one truly owns.

Here is the first concrete use of macroeconomics, and it owes nothing to prediction. Even if the market is perfectly efficient and you give up ever beating it, you need to understand the economy in order to know what your portfolio is exposed to — and therefore whether the risks it carries are the ones you mean to run. Knowing the real content of what one holds is not an expert's luxury: it is the first requirement of anyone who puts money to work.

Understanding is not predicting: learning to read the news

The second use is just as independent of prophecy. To understand the economy is to possess a grammar for reading events as they occur. Without it, the stream of news is mere anxious noise; with it, it becomes a text one deciphers.

To read, here, is first to know how to tell the expected from the surprise. When a figure lands and the market moves, the investor who has the grammar knows to ask the only right question: relative to what was it expected? He reads the gap, not the level. He is not taken in by a headline trumpeting a "record profit" followed by a falling stock, nor by a "frightening" inflation print that the market greets with a shrug because it was already discounted. This faculty — banal for whoever has grasped the first article's lesson, out of reach for everyone else — turns a baffling spectacle into an intelligible sequence.

To read is next to understand why one's own portfolio moves. In 2022, two investors watched the same screen turn red. The one who understood macro saw this: it is a rate shock, the rate that discounts the future — the "bottom of the fraction" from the first article — has just jumped; corporate profits have not collapsed; this is a repricing, not an economic apocalypse. The other saw only red and a falling number he could not explain. Those two will not act alike — and acting differently at that precise instant is worth infinitely more than any prediction.

To read is, finally, to be able to follow the conversation that dominates markets: the one they hold ceaselessly with the central banks. The first article showed it — prices spend their time anticipating monetary decisions; understanding why a single word from a central banker can move billions demands that same grammar. Without it, the most powerful engine of markets remains foreign to you — you suffer its jolts without hearing their cause. None of this is forecasting: it is interpretation. It does not tell you what will happen; it lets you understand what is happening, in real time, instead of enduring it. And understanding what is happening to one's money is the precondition for not reacting to it foolishly — which brings us to the heart of the matter.

The real adversary is yourself

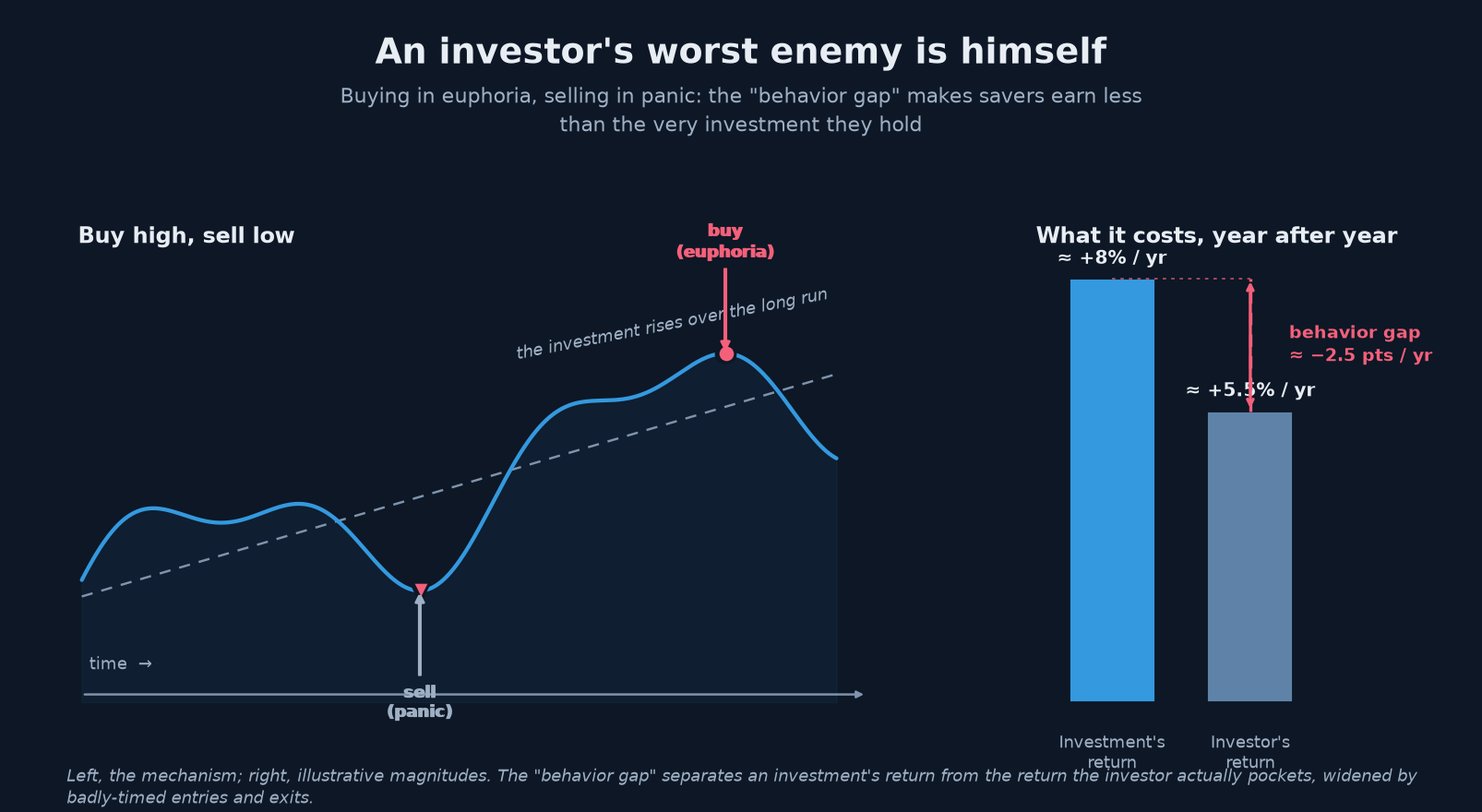

The saver's worst enemy is not the bad forecast: it is himself, at the moment everything wavers. The greatest destroyer of performance, measured and remeasured, is neither crashes nor crises, but the investor's behavior at the extremes — selling at the bottom, seized by panic; buying at the top, swept up in euphoria.

The figures speak plainly. Studies of how real individuals behave show that they earn less than the very funds they hold: they pour money in after the rises and withdraw it after the falls, so that their effective return falls short of the very investment they chose. The gap — what English speakers call the behavior gap — is the price of their own emotions. One can hold the right asset and lose all the same, simply by buying and selling it at the worst moment.

The "behavior gap": by buying after the rises, swept up in euphoria, and selling after the falls, seized by panic, the investor pockets a return below that of the very investment he holds. The gap comes not from the market, but from his own badly-timed round-trips. The most recent measurements put it at roughly one to two percentage points a year; the diagram exaggerates it on purpose for legibility.

It is here that understanding the economy reveals its least expected virtue: not to predict the fall, but to make it possible to live through it. The investor who knows that a 20% drop is the normal, expected behavior of equities in a tightening regime — that it is the price paid for the long-run return, not an anomaly — can hold, and even add into the decline. The one who does not understand sells at the worst moment and carves his loss in stone. Macro will not have told him the fall was coming; it will have given him the means not to flee it.

Above all it helps settle the only question that truly matters in the storm: is this an ordinary drop within a regime, or a change of regime? Most declines belong to the first case and are to be held, even bought; a few belong to the second and warrant real change. One cannot tell them apart without understanding the underlying economy — and it is there, on that discrimination, that the hard, legitimate, difficult core of macroeconomic judgment resides. The first article said it in its own way: the wisest response to a macroeconomic forecast is often to change nothing at all. Macro gives the conviction to do nothing when doing nothing is right, and to act when the regime turns for good. The one and the other, over the span of a saving life, are worth more than the finest prediction.

Efficiency does not make all portfolios equivalent

It remains to face the objection in its strongest form — "it's all already in the prices" — and to disarm it at the very point where it seems unanswerable. Let us grant it entirely. Suppose markets are perfectly efficient: every asset correctly valued relative to its risk, no free lunch anywhere, no anomaly to exploit. Does it follow that understanding the economy is useless? No — and grasping why is the keystone of this whole article.

Efficiency means one thing, and one alone: you cannot obtain more return without accepting more risk; you do not beat the market for free. It in no way means that all portfolios are equal. A thirty-year-old saving for retirement and a retiree drawing income from it should not hold the same allocation, even though they face the same efficient market — because their horizon, their capacity to absorb a bad regime, their needs differ. Choosing the right point on the scale of risk, choosing your exposure to growth, to inflation, to rates, is a decision the market does not make for you. The market sets the price of assets; it does not choose your portfolio. That choice is yours, and it is, irreducibly, a macroeconomic choice.

Concretely: should you hold protection against inflation? long bonds, highly sensitive to rates, or short ones? lean toward equities or keep cash? how far to diversify across regimes? None of these questions finds its answer in "the market is efficient." All find it in understanding the regimes one may face and the way each asset behaves in them. Efficiency sets the price of the menu; it does not compose your meal.

Now let us relax the assumption, for reality is less smooth. Markets are not perfectly efficient: the consensus scenario can be wrong for a long time, especially about slow regime shifts, which prices are sometimes late to absorb precisely because they are slow. In 2021 and 2022, markets and central banks long called inflation "transitory" and were wrong in concert, for a long time. But here is the decisive methodological point: the need to understand the economy does not rest on these imperfections. It would stand even if they never occurred. The inefficiencies are a bonus for the rare investor able to exploit them; knowledge of the climate, sight of one's exposures, the ballast that stays the hand — all that is a necessity for every investor, efficient market or not.

This is what finally dissolves the opening paradox. "It's all in the prices" answers the question "can I beat the market with macro knowledge everyone shares?" — and the answer is, most often, no. It answers nothing of the other question, the only one that matters to the saver: "do I need to understand the economy in order to invest well?" — and there the answer is an unreserved yes. The two questions were never the same; the beginner's whole error lies in their confusion.

Preparing rather than forecasting

From all this a posture emerges, the exact opposite of the soothsayer's. The forecaster bets on one future and is judged on its arrival. The investor must live in the future that actually comes — including the one he did not expect. His task is therefore not to predict but to prepare: to build something that holds in several possible worlds at once.

Macroeconomics is the tool of that preparation. It does not whisper which world will come; it maps the space of plausible worlds — the regimes — and indicates how the portfolio would behave in each. So armed, one stops asking "what is going to happen?" and asks the far better question: "if regime X arrives, am I ruined or merely uncomfortable — and is that a risk I can live with?" This is reasoning by scenarios, not by point prediction, and it transforms macro: from a forecasting machine, which it is poor at, into a robustness machine, which it excels at. The first article already put it: build a portfolio that withstands several scenarios rather than betting on one.

Hence the humility that must accompany this discipline, and that bears repeating to close: macroeconomics lights the set, it does not whisper the line. It will not make you rich quickly, and whoever promises that misunderstands it. What it offers is quieter and more lasting: knowing what you own, reading what happens, holding firm when others give way, and being built for more than one tomorrow. Over the length of a saver's life, that is worth more than a gift of prophecy.

The rest of the journey

The first article drew the map; this one has given the reason to walk it. Everything that follows — first the building blocks (growth and wealth, money, inflation, rates), then the dynamics (the cycle, employment, the indicators, the central banks), then macro wired to the markets — now has a purpose that is no longer to predict, but to understand the world one invests in, to see one's risks there, and to prepare for them. Each concept we study will find its place in that ambition.

The journey begins, logically, with the most fundamental building block: the wealth an economy produces, and the way we measure it — growth and gross domestic product. That is where the next chapter sets out. Before stepping into it, let us carry along the starting intuition that will have borne this one: understanding the economy does not serve to know what is going to happen, but to know what one is exposed to when it does — and it is that knowledge, not a gift of prophecy, that separates the investor from the one who merely bets.