Microeconomics and Macroeconomics: The Difference, with Concrete Examples

· 22 min read

One autumn, in a factory town, word of layoffs runs from workshop to workshop. A prudent worker draws the wisest lesson there is: he tightens his way of life, gives up the car he was eyeing, sets aside what he can, builds a cushion for the winter he senses coming. No one could fault him — it is exactly what a good adviser would recommend. But that winter, fear is everywhere, and every household in the country does precisely the same thing at the same moment: purchases are postponed, plans cancelled, money saved. Yet one person's spending is another's income. As all stop buying, firms sell less, trim their sails, lay off — and the recession each one feared, all of them together have deepened. Our prudent worker ends up losing the very job he meant to protect. No one was irrational; each did the right thing. It is their sum that went wrong.

This little story — economists call it the paradox of thrift, and we will return to it — contains in embryo the whole subject of this chapter. It shows something the intuition at first refuses to admit: what is true for one can be false for all. What shelters a lone household, generalized to the whole economy, can sink it. This is neither a sleight of hand nor an exotic case: it is the fault line that separates two ways of looking at the economy, and to cross it without seeing it is the most common — and most costly — error in all of economic reasoning.

These two ways of looking have names. Microeconomics observes individual decisions — a household, a firm, the market for a single good — and the way they adjust to one another through prices. Macroeconomics observes the economy taken as a whole — national output, the general price level, employment, interest rates. We usually believe the second is merely the first writ large, a simple change of scale: macro would be micro seen from afar, the sum of a very large number of individuals. This is false, and it is precisely the illusion this chapter means to dispel. A whole is not a big part; a crowd is not a big individual. Between the two lenses there is indeed a bridge — but it is narrow, and one breaks one's neck on it more often than one thinks.

For the investor, the stakes are anything but abstract. Almost every great interpretive error he will make — believing the economy is run like a household, that what he can do alone all can do together, that a good company makes a good investment whatever the climate — is, at bottom, the same error: applying to the whole a law that holds only for the part. Learning to tell the two lenses apart, knowing which to summon and when, is to guard against the confusion that ruins judgment at the worst moment. Let us see, then, with concrete examples, exactly where the border runs.

Two lenses, not two sizes

Let us begin with definitions, but refusing the lazy one that speaks only of size. One often reads that microeconomics studies "small units" and macroeconomics "large ones" — the consumer on one side, the nation on the other. The formula is not false; it is misleading, for it suggests a simple nesting: one need only stack enough consumers to obtain a nation. The reality is subtler.

Microeconomics studies how individual agents — a household allocating its budget, a firm setting its price and output, the buyers and sellers of a particular market — make their decisions and coordinate through prices. Its questions are precise and local: why does coffee cost what it costs? how does a pay rise change a household's choices? what happens to a city's housing market if rents are capped? Its sovereign method is to isolate one market and vary a single thing there while holding all the rest fixed.

Macroeconomics, for its part, studies the economy as a whole through its aggregates — magnitudes that sum up the activity of millions of agents in a single number: gross domestic product, which measures everything a country produces; the inflation rate, which condenses the overall movement of prices; the unemployment rate; the level of interest rates. Its questions are global: why does the whole economy accelerate, then slow? why do prices, in general, rise? why do millions of people find themselves out of work all at once?

The decisive difference is therefore not the size of the object but its nature. An aggregate is not merely "bigger" than an individual decision: it is of another species, because in adding individuals up one brings forth interactions that existed at no one's individual scale. My neighbor and I may both want to sell our house; if the whole neighborhood wants to sell on the same day, the price at which we sell is no longer the one each of us had in mind. The crowd brings forth a behavior that none of its members contained. That is the whole matter, and the rest of this chapter is merely its unfolding.

The original sin: the fallacy of composition

Let us give the error its name, for to name it is already to defend oneself against it. It is called the fallacy of composition: believing that what is true of a part is necessarily true of the whole. It has an inverse twin — the fallacy of division, believing that what is true of the whole is true of each part — to which we will return; but it is the first that haunts economics.

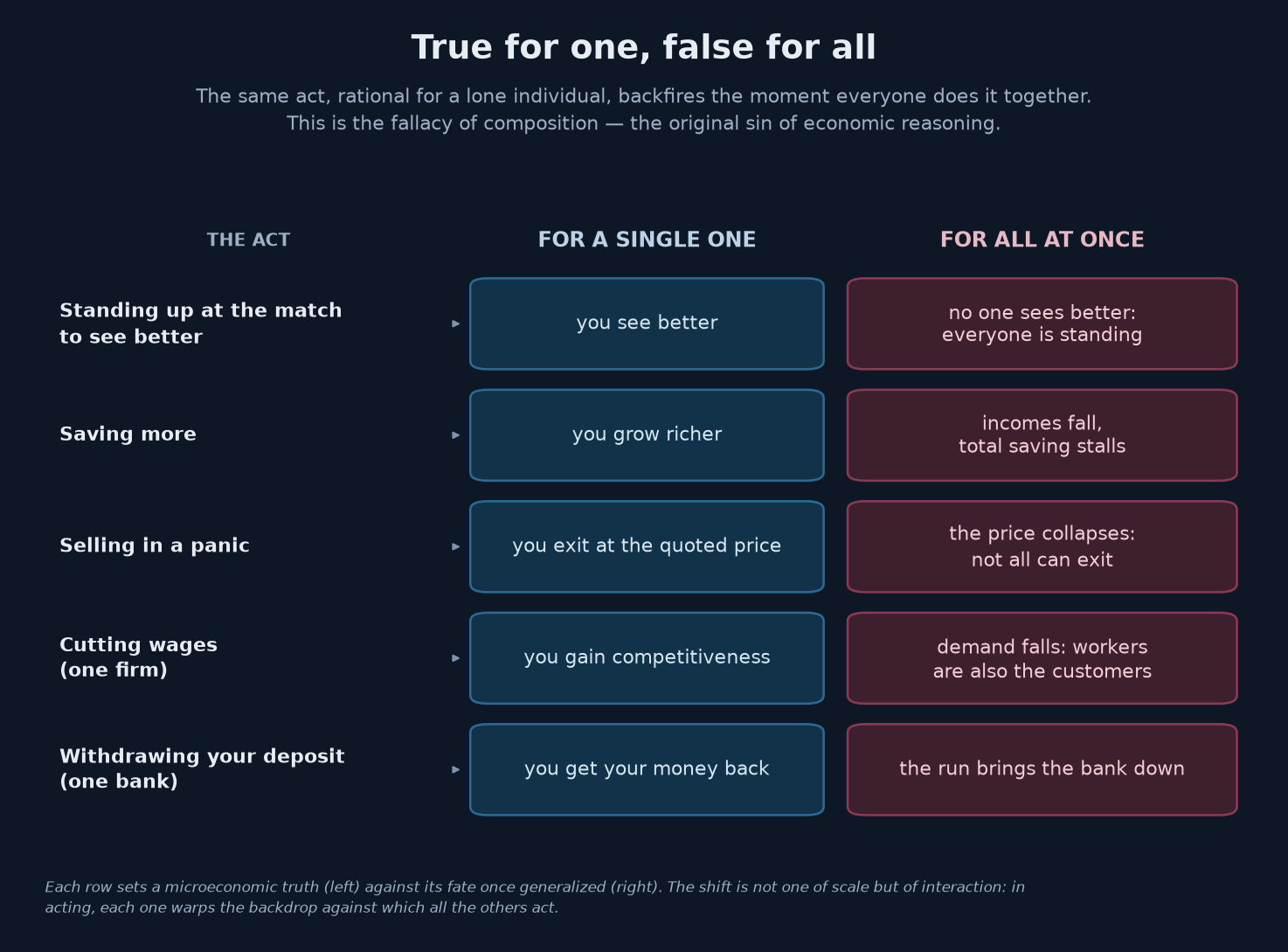

The clearest example is not economic at all. You are at the stadium, the play tightens, you stand up to see better. Excellent idea — for you. But your neighbor stands too, then the whole stand, and soon everyone is on their feet, no one sees any better than before, and everyone's legs ache. The act that gave you an advantage, once generalized, gives nothing to anyone: it merely shifts the equilibrium toward a state where all are standing and as badly off as when seated. Same structure on the highway on a holiday weekend: leaving an hour early to beat the traffic is shrewd as long as you alone think of it; if all think of it, the jam simply re-forms an hour earlier.

Why this reversal? Because at the individual's scale, the environment is a fixed backdrop: when I stand up alone, the stand stays seated; when I save alone, the economy keeps turning. My action is too small to warp the world it sits in, and I can legitimately reason "all else being equal." But when all act in concert, that backdrop ceases to be fixed: it is made of the sum of our actions. What each took for an immovable background becomes the moving result of what all do. The assumption that grounded individual reasoning — the rest does not move — is precisely the one that gives way at the collective level.

The same act, rational for a single individual, backfires the moment everyone does it together. Standing up at the match, saving, selling in a panic, cutting wages, rushing to withdraw a deposit: each row is true on the left and false on the right. The reversal owes nothing to scale and everything to interaction — in acting, each one warps the backdrop against which all the others act.

From this tipping point macroeconomics draws its reason for being. It is the science that refuses to hold the environment fixed, that doggedly tracks the loops micro allows itself to ignore. Where individual analysis stops at the first round — I save, so I grow richer —, macro pursues the second, then the third: I save, so another sells less, so his income falls, so he in turn saves less. It is these feedback effects, invisible at an individual's height, that make the whole difficulty — and the whole necessity — of the macroeconomic lens.

What is virtue for one may be vice for all

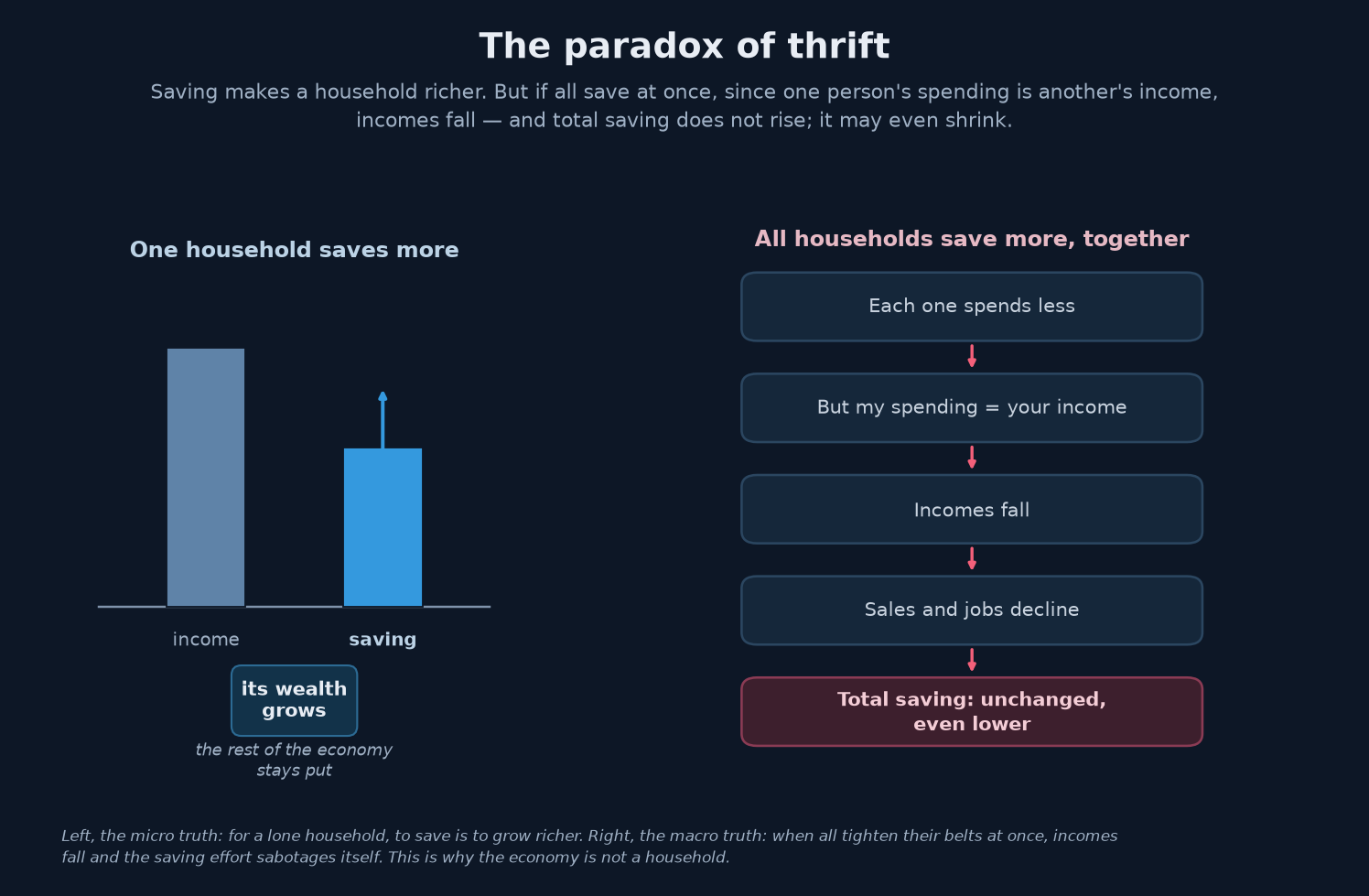

Let us return to our prudent worker and give his misadventure its full reach. The paradox of thrift, brought to light by John Maynard Keynes in the 1930s, says this: if a single household decides to save more, it grows richer, beyond dispute; but if all households decide to save more at the same moment, it may be that none succeeds, and that all grow poorer.

The mechanism rests on an accounting identity of formidable simplicity: my spending is your income. What I pay the baker is the baker's income; what I do not pay him is not. When a lone household cuts its spending to save, the effect on others' income is imperceptible — a drop in the ocean. But when all cut their spending together, the sum of those drops is a general fall in incomes. And one does not save out of an income that has evaporated: as incomes recede, the capacity to save recedes with them. At the end of the chain, the economy has contracted, everyone is poorer, and total saving has not risen — it may even have fallen. Each one's virtuous intention has produced a result no one wanted.

For a lone household, to save is to grow richer: the rest of the economy does not stir. But when all tighten their belts at the same moment, each one's lower spending is everyone's lower income — and the collective effort to save sabotages itself. This is the deep reason one cannot reason about an economy as about a family budget.

The same trap closes on wages, in a form that speaks directly to markets. For a lone firm, cutting wages is a tried-and-true way to regain competitiveness: its costs fall, its margins recover, it undercuts its rivals. But if all firms cut wages at the same time, something else happens: employees are also the customers. The purchasing power that bought the products collapses at the same time as the costs that made them. What was an advantage for one firm becomes, generalized, a depression of demand from which all suffer. Economists speak here of the paradox of costs: a wage is a cost for the employer but an income for the economy, and one cannot compress the one without amputating the other.

It is from this family of paradoxes that one of the most useful warnings to the investor comes: the economy is not a household. One hears the analogy constantly — a country should "tighten its belt like a family," "not spend more than it earns," "pay down its debts like you and me." The analogy is seductive and, applied to the whole, false: for when the government cuts its spending, it also cuts the incomes of those who lived off that spending — exactly like households all saving together. What is prudence for a family can be, at the scale of a nation and above all in the trough of a recession, a machine for making things worse. One may debate the magnitude of the phenomenon; one cannot ignore it without committing, precisely, a fallacy of composition. The investor who keeps this in mind reads economic policy — and the noisy debates around it — with a clarity many lack.

The individual cannot see the loop

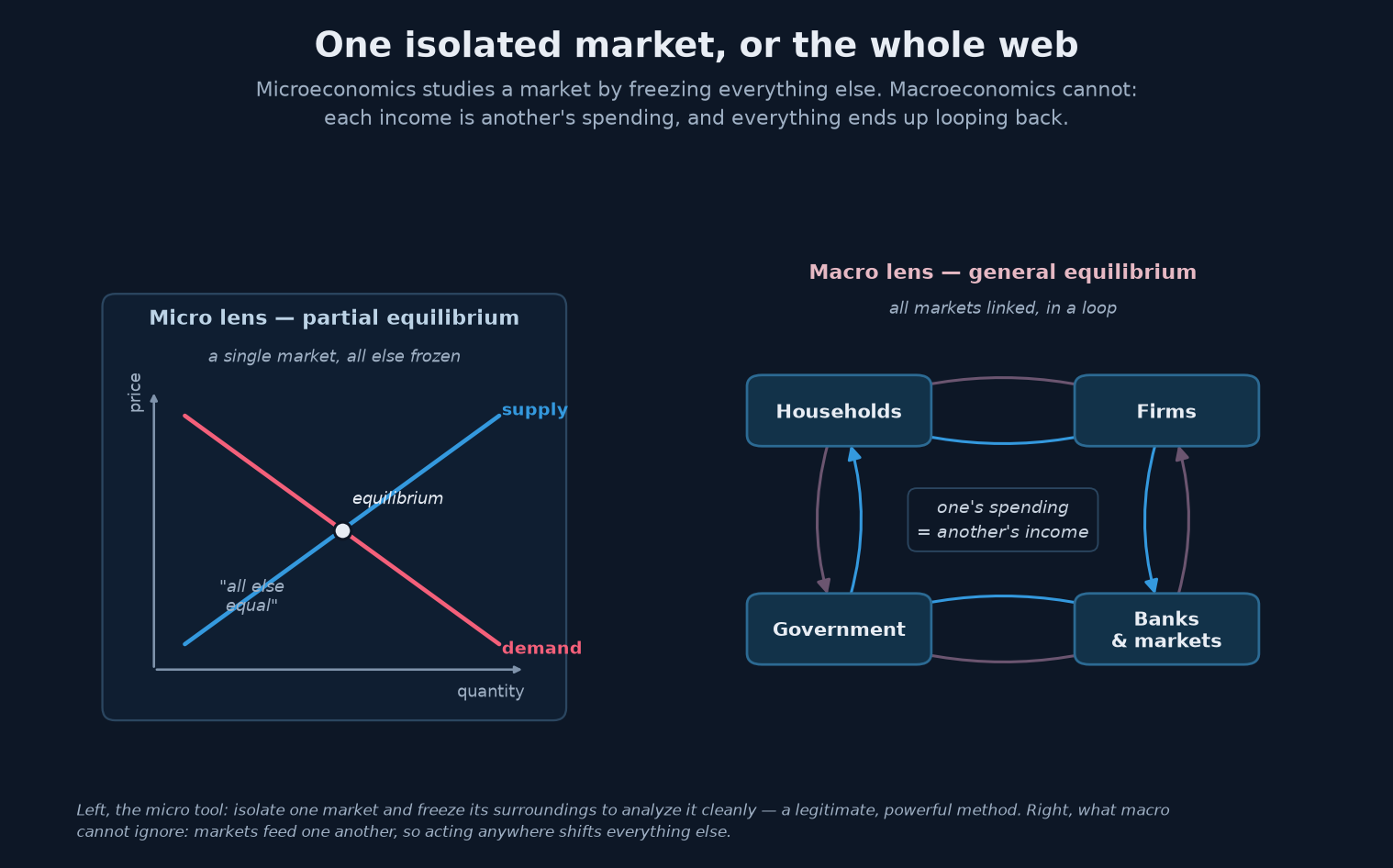

What these paradoxes have in common is a loop the individual cannot see from where he stands. Economists have a pair of words to name the difference of lens it imposes: partial equilibrium and general equilibrium.

The micro lens works in partial equilibrium: it isolates one market — apples, labor, housing — and analyzes it assuming all the rest of the economy stays unchanged. This is the famous "all else being equal," in Latin ceteris paribus. Far from a naïveté, it is a powerful and perfectly legitimate tool: to understand the effect of a tax on the tobacco market, it is reasonable to neglect what it changes in the car market. Isolating in order to understand is the ABC of every science.

But what is licit for a small market becomes misleading for the whole economy, for at that level there is no longer any "rest" to hold fixed: everything is the rest of everything. The macro lens must therefore work in general equilibrium, where each market is tied to all the others. A wage is a cost for the employer and an income for the employee; saving is a leakage out of spending and a resource for financing; a price is one party's revenue and another's expense. One cannot touch a single thread without the whole web quivering. To freeze the environment, here, is no longer to simplify usefully: it is to erase the very phenomenon one claims to study.

Micro isolates a market and freezes its surroundings to analyze it cleanly: a legitimate, fruitful method. Macro cannot — since each income is another's spending, acting anywhere shifts everything else. On the markets, this loop has a name: liquidity. One can sell alone at the quoted price; all cannot sell at once without collapsing that price.

The investor knows this loop under a very concrete name: liquidity. As long as you are small, you can reason in partial equilibrium — you buy or sell at the quoted price, and the market does not notice your passing; the price is, for you, a fixed backdrop. But the moment you carry weight, or the moment all want to do the same thing as you, that assumption collapses: you are no longer the spectator of the price, you are a component of it. A fund trying to liquidate a massive position drives down the very price it sought to capture; a crowd rushing for the exit discovers that the door is narrower than the room. It is the return, on the markets, of the stadium paradox: each can sell, but all cannot sell at the same time without collapsing the price at which they meant to. A crash is the fallacy of composition at work in real time.

There is even a further notch, peculiar to markets: not only does collective action shift the backdrop, but expectations shift it too. If all believe an asset will rise and buy it, it rises — their belief has manufactured the fact it announced. This reflexivity, where the gaze cast on the object alters the object, has no equivalent in the natural sciences: the planet does not care what the astronomer thinks of it, but the market does react to what investors believe of it. It is one more reason the macroeconomic loop never quite reduces to the sum of individual behaviors.

The whole has properties the parts do not

We must now take one more step and state what all this implies: the whole possesses properties that none of its parts possesses. Philosophers speak of emergence — the appearance, at the scale of the whole, of phenomena that make no sense at the scale of the element.

Take inflation. An individual does not "make" inflation; he cannot be "at 3% inflation." Inflation is an overall movement of the price level, a property of the entire system, born of the way money, expectations and millions of pricing decisions interweave. Likewise unemployment, growth, the business cycle: these are not attributes one could read off a lone individual, they are states of the collectivity. Money itself is an emergent object: a banknote has value only because all agree to lend it value — its worth is not in the paper, it is in the coordination of all. Remove the collective belief and only a printed scrap remains. No analysis of the individual alone will ever account for what money is.

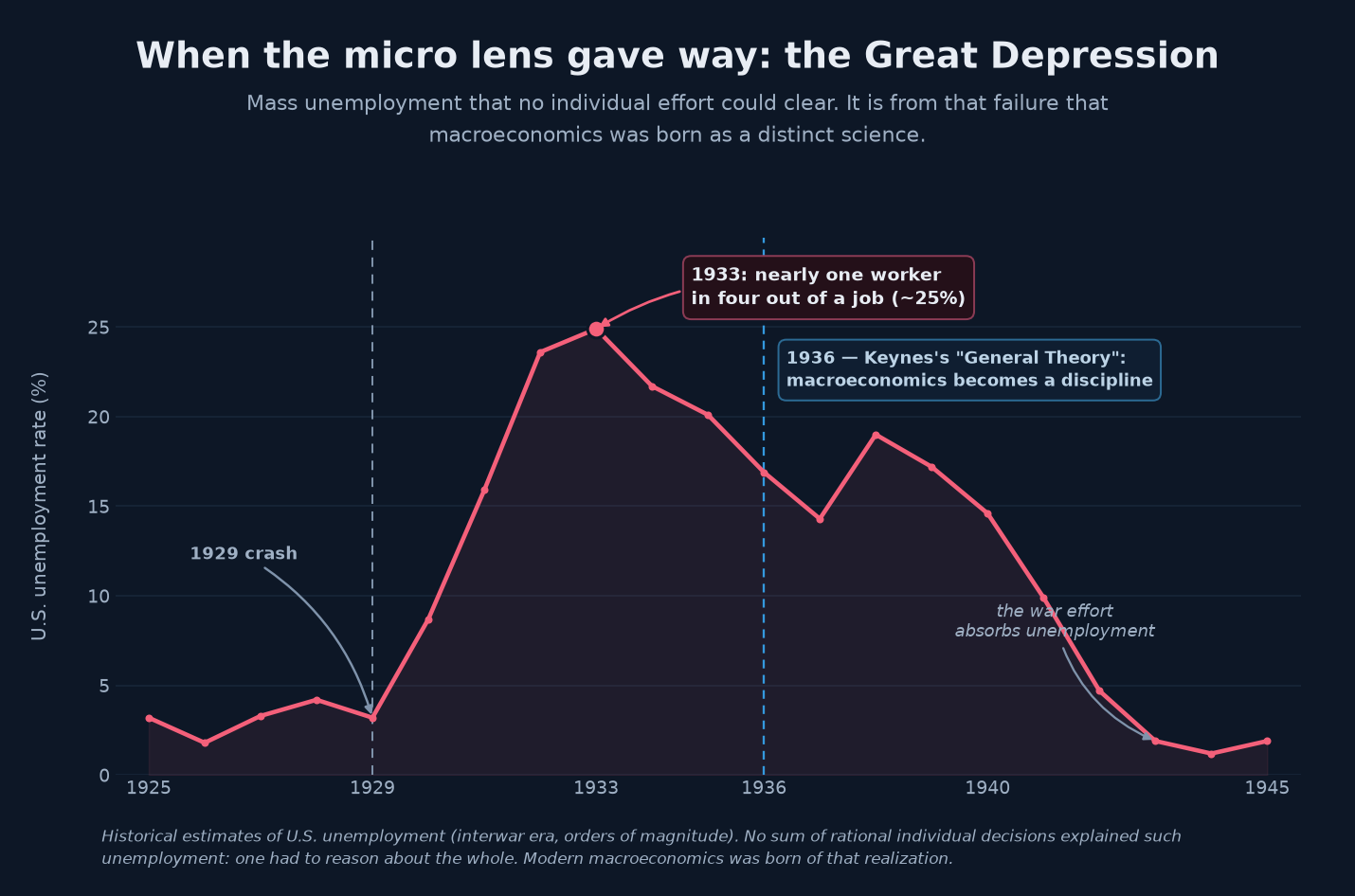

The gravest example, historically, was unemployment. The micro lens tells a reassuring story: a labor market like any other, where the wage adjusts until supply equals demand; if unemployed remain, it is because the wage is too high, and it would suffice for it to fall for everyone to find work again. That story, plausible for a particular trade in a particular town, shattered on the Great Depression.

Mass unemployment — nearly one worker in four — that no individual decision could explain or clear: the wage might well try to fall, but aggregate demand had collapsed. One had to reason about the whole. It is from this failure of the micro lens that macroeconomics was born as a distinct science.

At the trough of the 1930s, a quarter of the American labor force was out of work — not by choice, not because these people refused to work at the going wage, but because aggregate demand had collapsed and no individual effort could do anything about it. A jobless worker might well accept a lower wage; he only shifted the problem onto another; and if all accepted lower wages, one fell back into the paradox of costs — less purchasing power, less demand, still more unemployment. The whole was caught in a trap that none of its parts could loosen alone. It is this realization, precisely, that gave birth to modern macroeconomics: it had to be admitted that the economy taken as a whole obeyed laws of its own, laws one could not deduce from individual behavior alone. Keynes's General Theory, in 1936, marks that birth — the micro lens, on its own, had given way.

The fragile bridge between the two

Should we conclude that micro and macro are two worlds without communication, two sciences foreign to each other? That would go too far, and modern economics works precisely to throw a bridge between them. That bridge has a name: microfoundations. The ambition is legitimate and fine — to rebuild macroeconomic magnitudes from the decisions of optimizing individual agents, so that macro is not suspended in mid-air but rooted in intelligible behavior.

The enterprise is fruitful, but it runs into a difficulty this whole chapter has prepared: the problem of aggregation. Passing from individuals to the whole is not a simple addition, because it is precisely the interactions — the loops, the coordination, the crossed expectations — that make the whole. The convenient shortcut of the representative agent, which treats the economy as if it were peopled by a single average individual cloned a thousand times, does away by construction with what makes macroeconomics: a single agent knows neither the paradox of thrift, nor bank runs, nor involuntary unemployment, for all of these presuppose that agents are different and get in each other's way. One can build the bridge, but one must beware of believing it has removed the river.

Here one must guard against the symmetrical error, the other face of the fallacy of composition: the fallacy of division, which consists in believing that what holds for the whole holds for each part. "Growth was 3% this year, so I grew 3% richer": no — the average may well mask that most stagnated while a minority grew rich. "The market returned 8%, so I earned 8%": no again, and the previous chapter showed it with the behavior gap. Descending from the whole to the individual is as perilous as climbing from the individual to the whole; both journeys cross the same minefield.

The right position, then, is not to prefer one lens to the other, but to know which suits which question. Micro is right about the tree, macro about the forest — and a forest is not a big tree. Whoever studies a tree with the forest's tools misses it, and vice versa. The whole skill lies in never applying to the whole a law that holds only for the part, nor to the part a law that holds only for the whole.

What the investor must take from this

Let us now bring all this back to money, for that is where the distinction, so abstract in appearance, becomes an instrument. Three lessons, at least, follow directly.

The first: never reason about the market as about a big individual. You can sell; all cannot sell at the same time. The exit is narrower than the room. This one truth, held firmly, protects against the two most classic traps — believing one will always be able to liquidate at the quoted price on the day everyone wants to, and being surprised that correlations "break" exactly when they are most needed, as in 2022. It is not an anomaly: it is the fallacy of composition presenting its bill.

The second: never reason about the economy as about a household. The great debates that shake markets — is public debt sustainable? does austerity cure or worsen a recession? is a stimulus a waste or a support? — remain incomprehensible as long as one maps them onto the intuition of a family budget. Armed with the paradox of thrift, the investor sees what the domestic analogy hides, and listens with a critical ear to anyone who sells him one or the other certainty as plain common sense.

The third: always know which floor you are reasoning on. A micro claim — "this company is excellent and cheap" — and a macro claim — "this rate regime is hostile to this kind of company" — are two distinct propositions, calling for distinct tools, and can both be true at once. The finest stock selection in the world can be swallowed by the wrong macroeconomic climate, like the finest growth stocks in 2022; this is the direct link with the previous chapter, where we saw that every portfolio is a macro bet that doesn't know it. To tell the micro floor from the macro floor is to stop confusing "I am right about the company" with "I will be right about the investment."

Key takeaway — Microeconomics and macroeconomics are not the same science at two scales: what is true of an agent can be false of the whole, because in acting each one warps the backdrop against which all the others act. The error is not to use one lens or the other — both are right in their place — but to apply to the whole a law that holds only for the part. Almost every great blunder in reasoning about money lies in that single confusion.

The rest of the journey

This chapter has not added a brick to the edifice: it has set the focus before we begin to build. We now know at which level we will stand throughout this journey — that of the whole, of the economy taken in one block — and why that level obeys laws of its own, irreducible to the sum of individual behaviors. It is the macroeconomic lens itself that we have just brought into focus.

There remains the first stone to lay. Since macroeconomics looks at the economy as a whole, its very first task is to measure that whole: how much, exactly, does an economy produce, and how does one add up cars, haircuts and software into a single figure? This founding aggregate, from which nearly all the others flow, bears a name everyone has heard without always knowing what it covers: gross domestic product. It is with it, and with the growth that makes it vary, that the next chapter opens. Before stepping into it, let us keep the intuition this one leaves us: an economy is not an individual writ large, and most errors about money begin the day one believes that a whole obeys the rules of its parts.

Sources and further reading

- John Maynard Keynes, The General Theory of Employment, Interest and Money (1936) — aggregate demand, the paradox of thrift, and the birth of macroeconomics as a discipline.

- Michał Kalecki, Essays in the Theory of Economic Fluctuations (1939) — the mechanism of the paradox of costs: cutting wages everywhere at once depresses demand instead of lifting profits.

- Paul A. Samuelson, Economics (1948) — the introduction of the fallacy of composition and the paradox of thrift into mainstream economic analysis.

- Stanley Lebergott, Manpower in Economic Growth: The American Record since 1800 (1964) — the historical series of the interwar U.S. unemployment rate used in the figure; supplemented by the Bureau of Labor Statistics reconstructions (Labor Force, Employment, and Unemployment, 1929-39).

- Marc Lavoie, Post-Keynesian Economics: New Foundations (2014) — a synthesis of the macroeconomic paradoxes (composition, thrift, costs) and the critique of the representative agent.